2022-01-08

Enthusiastic pursuit of expanded natural gas production from the North West Shelf by Woodside seemingly overlooks a host of downside risks, with stranded assets looming as the likely outcome

By Mark Brogan, member of the Climate Change Working Group, Greens WA

With output from its existing North West Shelf and Pluto gas fields in decline, LNG gas giant Woodside has spent a decade looking for new production capacity. On November 22, 2021 it announced an end to this quest, committing to the development of the Scarborough gas field and a new LNG train at the Pluto LNG processing facility, some 400 km from the field.[1]

Capital costs were estimated at $16 billion with an output of 8 million tonnes of LNG per annum.[2] Projected Greenhouse Gas Emissions (GHG-e) (Scope 1 & 3)[3] are the subject of a bun fight with estimates ranging from 880 million tonnes (Woodside)[4] to 1.6 billion tonnes (Conservation Council of WA).[5] While Woodside claims that its emissions profile aligns with the 1.5°C Paris agreement goal, analysis done by science and policy analysts, Climate Analytics, contradicts this claim.[6] Climate Analytics puts emissions from Scarborough at 1.37 billion tonnes equivalent to an effective 12% increase to WA's 2005 emissions and a 2% increase to Australia's total emissions.[7] The most serious consequences for global warming will come from downstream Scope 3 emissions including emissions from consumption in Australia’s LNG export markets. Deflecting criticism on the Scope 3 emissions issue, Woodside has said that it will have more to say about Scope 3 emissions in 2022. Divestment has also been touted as an available option to concerned shareholders.[8]

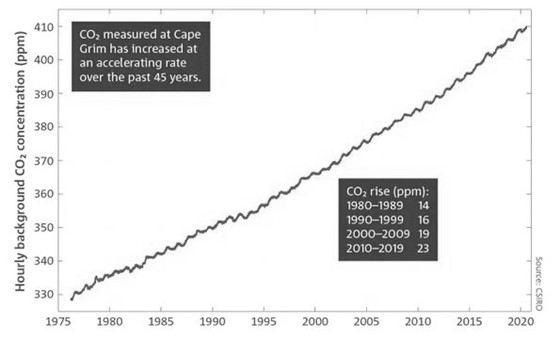

While Woodside spent a decade agonising over how to remain a player in world LNG markets with declining output from its existing fields, the relentless, deterministic physics of global warming and climate change were working to re-shape our relationship with the biosphere. Australia plays a role in international efforts to measure emissions through the Cape Grim monitoring station located on the northwest tip of Tasmania. The following chart of CO2 emissions measured at the station shows an accelerating rate of atmospheric concentration of CO2. The decade 2010-2019, in which Woodside mulled over what to do, involved a near doubling the rate of increase in atmospheric CO2 concentration, relative to the first decade after establishment of the monitoring station. (Fig.1)

Figure 1- Atmospheric CO2 (ppm) 1975-2019 Source: CSIRO

With accelerating growth in atmospheric CO2, extreme weather events are increasing in frequency and severity across the globe.[9] Ocean warming is endangering reef systems and threatening communities and nations through sea level rise.[10] The likelihood of mass species extinction arising from failure to adapt to rising temperature and habitat change is also real. Extreme weather events operating over large geographic areas add to risk. In 2019-20, an estimated 3 billion animals died in the catastrophic Black Summer bush fires in NSW and Victoria.[11] The fires burnt an area of 1.8 million hectares and released 715 million tonnes of CO2 into the atmosphere, 200 million tonnes more than the amount produced in human activity in Australia in 2018.[12]

Growing alarm about the consequences of a global temperature increase above 1.5 °C relative to pre-industrial levels led to the signing of the Paris Agreement in 2015, by one hundred and ninety-six (196) party nations to the UN Framework Convention on Climate Change (UNFCCC). In the Paris Conference of Parties (COP21) nations agreed a legally binding international treaty on climate change with the explicit goal of limiting global warming to well below 2°C, preferably at 1.5°C compared to pre-industrial levels. At COP26 in Glasgow in November 2021 one hundred and fifty-three (153) countries updated their emissions targets (NDCs) for 2030, describing greater emissions reduction ambition. A further one hundred and ninety (190) agreed to phase down coal power. Nations also agreed to halt and reverse deforestation (137) and to speed up the switch to electric vehicles (30). One hundred (100) countries agreed to reduce methane emissions.[13]

Australia's maverick, regressive position on climate was on clear view in Glasgow, where the Australian Government:

- Declined to raise Australia’s 2030 emissions reduction target (26%-28% on 2005 with LULUCF).

- Declined to sign on to a global pledge to reduce emissions of methane (a more potent GHG gas). The pledge was signed by one hundred (100) other countries.

- Pushed the barrow on gas as a transition fuel despite scientific evidence suggesting only marginal, if any, mitigation benefits.

- Worked in the background to water down the language on ending coal power.

Encouraged by the Morrison and McGowan Governments' collective tin ear on climate policy, Woodside can anticipate no Australian regulatory threat to its Scarborough ambitions. Far from it. Scott Morrison is reputed to have ‘danced a jig’ on being told of Woodside's investment decision.[14] The McGowan Labor Government in WA has also come to the party, foreshadowing enabling legislation should court action by the Conservation Council WA (CCWA) and Environment Defenders Office (EDO) succeed at blocking the project.[15]

With more than one hundred fossil fuel projects on the table for approval, and no buy into the headline changes agreed by others at COP26, the Australian Government expects and needs international resolve on climate change and emissions to fail. With this goal in mind, it played a quiet but obstructive role at Glasgow and is working actively in other contexts to preserve and grow markets for Australian fossil fuel exports. It is also moving to enhance domestic markets, by frustrating the energy transition and privileging fossil fuels in energy market regulation.

In summary, Australia is the petulant mouse that has roared and railed to ensure a future for fossil fuels in a changing world in which most nations want to decarbonise. Betting on the failure of global efforts to decarbonise is a huge risk for Australia’s LNG industry and for the Australian economy more generally. The bet involves huge opportunity costs arising from the potential wastage of economic resources on ‘gas led recovery’, resources that might have been used for the energy transition and development of new green industries. With around one hundred fossil fuel projects across Australia at various stages of approval, opportunity costs are nothing short of eye watering. For Santos, Woodside and other stakeholders in Morrison’s dream of a gas led recovery, if supply and demand projections for Australian gas are not realized, fallout involves swathes of production capacity intended to operate for fifty years, becoming legacy within ten to fifteen.

The ratcheting up of risk can also be seen in investor attitudes to LNG investment. Following the money on energy investment in Australian LNG shows increasing investor scepticism fuelled by competition from low-cost renewables, decarbonisation and the intensification of competition in global markets as new production capacity is added. The current buoyant situation of LNG exports outward to 2025, belies rapidly changing fundamentals and high uncertainty in markets from 2030 onwards.[16] Subsidies and domestic offtake deals to the LNG industry also describe liabilities to State and Federal Governments and, ultimately, to Australian taxpayers. Woodside’s Scarborough and Pluto expansion will increase domestic gas availability from 25T/day to 250 TJ/day, a massive ten-fold expansion that will add 20% to WA’s projected gas supply over the next decade, crowding out action on decarbonisation.[17]

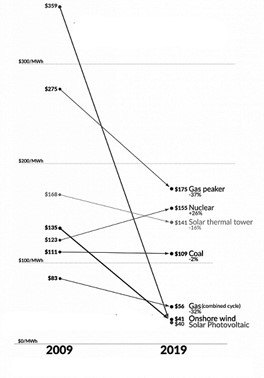

Meanwhile, displacement of gas by renewables in electricity markets is proceeding at pace. In Australia in the first half of 2021, renewable energy (wind and solar) supplied 28.8% of electricity to Australia’s main grid.[18] In the same period, gas generators supplied 6.1 per cent, with most generation occurring in just two states.[19] Gas use for power generation was down 2% on 2020. International trends are similar. International Energy Agency (IEA) reports that in 2020, renewables global share of electricity generation was 29% and expects that in 2021, renewable electricity generation will expand by 8% to reach 8300 TWh, the fastest year on year growth since the 1970s.[20] Figure 2 shows the 2019 Levelized Cost of Energy (LCOE) used to produce electricity ($/MWh) using different energy sources. The chart shows that by 2019, on shore wind and solar photovoltaic overtook all forms of gas-based electricity generation.

Figure 2- Levelized Cost of Energy ($/MWh) by feedstock Source: OurWorld in Data[21]

The stats on cost reduction are breathtaking. In the ten years from 2009 to 2019, LCOE of onshore wind declined by 70%. In the same period, LCOE of utility scale solar declined by 89%. The cost advantage that renewables had achieved by 2019, translated into effective market dominance with renewables accounting for 72% of all new capacity added in 2019. Importantly, by 2019, wind and utility scale solar pv had achieved clear price advantage compared with gas. Like coal, gas is highly susceptible to market disruption by renewables in power generation. It is also susceptible in other markets where it can be substituted for a low or zero emissions feedstock such as hydrogen, or where a thermal application can be electrified, with electricity sourced from clean energy sources.

Substitution and price competitiveness are not the only risks facing Scarborough. On the supply side, over supply looms with other LNG projects contemporaneous with Scarborough coming on stream in Qatar, the United States and Russia. The US is expected to supplant Australia as the world’s biggest LNG exporter by 2025.[22] Industry analysts Wood Mackenzie point to the likelihood of a supply glut in the mid-2020s led by Qatar.[23]

On the demand side, commitments made by Australia’s principal LNG customers to decarbonise in line with Paris and Glasgow goals, describe demand side contraction. As noted in the discussion of supply side factors, this contraction will occur in circumstances of new supply coming on stream, delivering an effective ‘double whammy’ to producers. Implications of the Paris 1.5º C goal for LNG markets, have been modelled by Climate Analytics using net zero pathways (IEA, Reserve Bank of Australia) and country specific scenarios.[24] The analysis shows significant over supply relative to net zero and country specific reduced demand outcomes as countries move to implement emissions reductions commitments. Reductions are expected to be rapid after 2030.[25]

Decarbonisation in line with the Paris Agreement goal, increased competition and oversupply are all working to ratchet up risk in Australia’s long standing LNG markets from the mid-2020s. Australia sells most of its LNG to China, Japan and South Korea. In December 2021, these three markets accounted for 52% of Australia’s total LNG exports.[26] Analysis shows that in each of these markets, demand side shocks are looming.

For example, in Glasgow, China committed to a net zero target of 2060. Compounding the impacts from decarbonisation, China is shifting its buying behaviour in favour of the United States and Qatar.[27] Until 2020, China had been reluctant to buy LNG from the US, but with concessions necessary under Trump’s US China trade deal, the door opened. Trade trouble with Australian LNG is also brewing as a consequence of the Australia-China antagonism, which has made contracting to buy Australian LNG problematic in China. Bloomberg reported in May 2021 that smaller Chinese importers had been instructed not to buy from Australian exporters.[28] The Australian Strategic Policy Institute (ASPI) concludes that the US will gain market share in China at the expense of Australia.[29] A medium term prognosis is that the US could soon be eating Australia’s lunch on LNG.

South Korea and Japan both increased emissions ambition as measured by NDCs at COP26. In addition to decarbonisation, downward pressure on LNG imports in Japan is coming from nuclear reactor restarts and increased renewables capacity. IEA expects Japanese imports to reduce by 10bcm/y to 2025.[30] IEA also expects South Korean LNG imports to ease, with the addition of 5.6 GW of nuclear and 7.3GW of coal by 2023.[31]

Other elements of risk for Woodside and Scarborough/Pluto include:

- Inherited liabilities relating to its schema of agreement with BHP to finance the Scarborough deal.[32]

- Projected increases in carbon abatement and carbon pricing costs over the life of the Scarborough project.[33]

- Fundamentals of its proposed Hydrogen (H2) Perth Project. The Scarborough Pluto project will add 20% to WA’s domestic gas supply, some of which will be used to produce blue hydrogen as part of the H2 Perth Project. Carbon border tariffs, preference for green hydrogen and cost competition from green hydrogen by 2030, can be expected to impact on viability of the $1 billion H2 Perth Project.[35, 36]

- Over reliance on offsets and Carbon Capture and Storage (CCS), the latter beset by a “history of failures, cost overruns and major deployment delays.”[37]

Conclusion

In a captured regulatory environment in which Australian Governments are pursuing the objective of a gas led recovery, the real dangers to Woodside's $16 billion Scarborough development are lurking elsewhere. They are found in the likelihood of increased competition from other LNG exporters, substitution, oversupply, price competition from renewables and in the demand reduction implications of more aggressive global decarbonisation. Intensification of these risks can be expected around the time Scarborough comes on stream in mid 2020s. Australia’s antagonism with its second largest market, China, also presents as a strategic risk to market share, as China shifts its LNG purchasing behaviour to buy more gas from the US. Further complications exist in a flawed plan to produce blue hydrogen, the rising costs of carbon credits and inherited liabilities from the BHP Woodside deal.

Such risks are currently being played down by the company, as it develops and refines its narrative around LNG forming a necessary ‘transition fuel’ to a low carbon world. But the risks are real and growing, pointing to the halcyon days of gas being over. If this is true, the Scarborough decision will be seen in hindsight as a Kodak moment for Woodside, capping a decade in which Woodside might have been using its profitability to position itself as a constructive player in the energy transition and global effort to combat climate change.

Potentially caught out by market disruption that might and should have been anticipated, Woodside shareholders will have much to think about when they vote on the investment decision in 2022.

ENDNOTES

[1] Milne, P. (2021). Woodside approves massive LNG project as $40bn BHP deal inked. Retrieved from https://www.watoday.com.au/business/companies/woodside-approves-massive…

[2] Petroleum Australia. (2021). Woodside approves Scarborough and Pluto Train 2 developments. Retrieved from: https://petroleumaustralia.com.au/projects/woodside-approves-scarboroug…

[3] Scope 1 and 2 emissions relate to those directly or indirectly generated from a company's operations while Scope 3 includes greenhouse gases emitted during consumption of a company's products.

[4] Readfearn, G. (2021). How high will emissions be from Woodside’s giant new gas project in Western Australia? The Guardian, 25November, 2021. Retrieved from: https://www.theguardian.com/environment/2021/nov/25/how-high-will-emiss…

[5] Ibid.

[6] Climate Analytics. (2021). Woodside’s Scarborough and Pluto Project undermines the Paris Agreement. Retrieved from: https://climateanalytics.org/publications/2021/warming-western-australi…

[7] Climate Analytics (2021). Warming Western Australia: How Woodside’s Scarborough and Pluto Project undermines the Paris Agreement. Retrieved from: https://climateanalytics.org/latest/woodsides-scarborough-lng-expansion…

[8] Butler, B. (2021). Shareholders pressure Woodside over carbon emissions and Scarborough gas project. The Guardian, 15 April 2021. Retrieved from: https://www.theguardian.com/australia-news/2021/apr/15/shareholders-pre…

[9] Samenow, J. & Patel, K. (2021). Extreme weather tormenting the planet will worsen because of global warming. The Washington Post, 9 August, 2021. Retrieved from: https://www.theguardian.com/australia-news/2021/apr/15/shareholders-pre…

[10] Waskow, D. & Gerholdt, R. (2021). 5 Big Findings from the IPCC’s 2021 Climate Report. Retrieved from: https://www.wri.org/insights/ipcc-climate-report

[11] Slezak, M. (2020). 3 billion animals killed or displaced in Black Summer bushfires, study estimates. Retrieved from: https://www.abc.net.au/news/2020-07-28/3-billion-animals-killed-displac…

[12] Smith, B. (2021). Black Summer bushfires triggered Southern Ocean algal blooms bigger than Australia. Retrieved from: https://www.abc.net.au/news/science/2021-09-16/black-summer-bushfires-s….

[13] UN Climate Change Conference (2021). COP26 The Glasgow Climate Pact. Retrieved from: https://ukcop26.org/wp-content/uploads/2021/11/COP26-Presidency-Outcome…

[14] Hastie, H. and Milne, P. (2021). Government ‘just rolls’ to WA gas industry without scrutinizing climate concerns: Corporate advocate. WAToday, November 30, 2021 Retrieved from: https://www.watoday.com.au/national/government-just-rolls-to-wa-gas-ind…

[15] Mazengarb, M. (2021). WA Premier vows to protect Scarborough gas project as Morrison dances jig of joy. Retrieved from: https://reneweconomy.com.au/wa-premier-vows-to-protect-scarborough-gas-…

[16] BloombergNEF. (2021). Global LNG outlook 2021-25 overview. Retrieved from: https://www.bloomberg.com/professional/blog/global-lng-outlook-2021-25-…

[17] Climate Analytics (2021) op.cit. p.1

[18] Mazengarb, M. (2021). Gas generation slumps in first half of 2021 as wind and solar continue to shine. Renew Economy 21 July 2021. Retrieved from: https://reneweconomy.com.au/gas-generation-slumps-in-first-half-of-2021…

[19] ibid

[20] International Energy Agency. (2021). Global Energy Review 2021: Renewables. Retrieved from: https://www.iea.org/reports/global-energy-review-2021/renewables

[21] Roser, M. (2020). Why did renewables become so cheap so fast? Retrieved from: https://ourworldindata.org/cheap-renewables-growth

[22] International Energy Agency. (n.d.) Gas 2020. Retrieved from: https://iea.blob.core.windows.net/assets/555b268e-5dff-4471-ac1d-9d6bfc…

[23] Wood Mackenzie (2021). Woodside sanctions US$12 billion Scarborough and Pluto Train 2 Project. Retrieved from https://www.woodmac.com/press-releases/woodside-sanctions-us$12-billion…

[24] Vide Climate Analytics. (2021). WA’s LNG Export Market Under Paris Agreement Implementation. In Warming Western Australia: How Woodside’s Scarborough and Pluto Project undermines the Paris Agreement. pp.59-68

[25] Ibid, p.3

[26] Australian Government. Department of Industry. (2021). Resources and Energy Quarterly, June 2021. Gas. Retrieved from: https://publications.industry.gov.au/publications/resourcesandenergyqua…

[27] Fowler, E. (2021). LNG shipments dip, China snubs Australia for extra supplies. The Financial Review, October 24, 2021. Retrieved from: https://www.afr.com/companies/energy/lng-shipments-dip-china-snubs-aust…

[28] Stapczynski, S. (2021). China Targets Some Australian LNG as Trade Dispute Widens. Retrieved from: https://www.bloomberg.com/news/articles/2021-05-10/china-targets-some-a…

[29] Uren, D. (2021). Australia could lose out from geopolitical machinations over global gas supplies. Australian Strategic Policy Institute. Retrieved from: https://www.aspistrategist.org.au/australia-could-lose-out-from-geopoli…

[30] International Energy Agency. (n.d.) Gas 2020, p.55. Retrieved from: https://iea.blob.core.windows.net/assets/555b268e-5dff-4471-ac1d-9d6bfc…

[31] Ibid., p.55

[32] Milne, P. (2021). Woodside approves massive LNG project as $40 billion BHP deal inked. WAtoday, 22 November, 2021. Retrieved from: https://www.watoday.com.au/business/companies/woodside-approves-massive…

[33] Vide Milne, P. (2021). Woodside’s two emissions tales crash and burn. WAtoday, December 16, 2021. Retrieved from: https://www.watoday.com.au/business/companies/woodside-s-two-emissions-…

[34] Risk is greatest when carbon pricing of Scope 3 emissions is factored into costs. For a discussion of the implications of carbon pricing on Scope 3 emissions, see Climate Analytics (2021). Warming Western Australia: How Woodside’s Scarborough and Pluto Project undermines the Paris Agreement. p.37. Retrieved from: https://climateanalytics.org/latest/woodsides-scarborough-lng-expansion…

[35] Milne, P. (2021). Woodside eyes $1b gas and renewable hydrogen plant near Perth. WAtoday October 25, 2021. Retrieved from: https://www.watoday.com.au/business/companies/woodside-eyes-1b-gas-and-…

[36] IRENA (2020). Green hydrogen cost reduction: Scaling up electrolysers to meet the 1.5 º climate goal. Retrieved from: https://www.irena.org/publications/2020/Dec/Green-hydrogen-cost-reducti…

[37] Climate Analytics. (2021). Op.cit. p.2.

Header photo: Bright flame tower of LNG gas plant lights the landscape with rising moon. Marius Fenger (2017). Licensed under CC.

[Opinions expressed are those of the author and not official policy of Greens WA]