2026-05-05

LNG: Labor, Japan and the Iran War

By Mark Brogan, Climate Crisis Working Group, Greens WA

Acknowledgement: Thanks to Geoff Bower for contributed content on the role of gas in the energy transition.

Labor likes to project a benign view of itself as a partner in global action to prevent dangerous climate change. But the reality is very different. Often covertly, under the cover of gas as a necessary enabler of the energy transition, Federal and State Labor are working with major gas companies to expand markets for Australian gas in southern and south east Asia, with potentially devastating consequences for global warming. As a re-seller of Australian gas, Japan has become an important partner in the push to addict Asian nations to Australian gas.

The consequences of this are huge for a world that is meant to be de-carbonising to avoid catastrophic climate change. The war with Iran is also likely to provide impetus to the development of new Australian gas.

LNG market trends in Asia

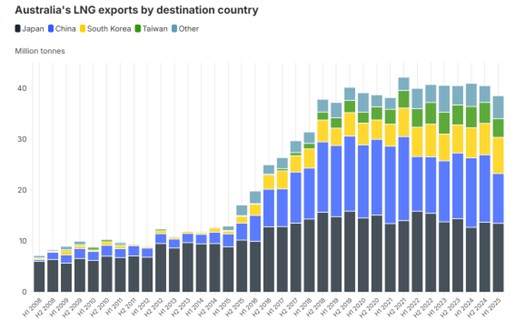

Australia has consistently performed as a top three gas exporting nation over the past decade. In the first half of 2025, LNG exports accounted for around 83% of Australia’s gas production, with only 17% used domestically.[1] By volume LNG exports to Asia have underpinned massive expansion of Australia’s LNG markets. However, export destinations and market shares have recently changed. Historically underpinned by China, LNG exports to China fell by 28% in 2025 compared with 2024. In the same period Taiwan recorded a 13% decrease. This was partly offset by a 20% increase in exports to South Korea, a 6% increase to Japan, and a 38% increase to other markets (albeit from a lower base).[2] In the 2024-25 FYR, the biggest markets for Australian gas were: Japan (1,504PJ or 27%), China (1,277PJ or 23%), the Australian domestic market (925PJ or 16%), South Korea (738PJ or 13%), Taiwan (429PJ or 7.6%), and other LNG exporters (350PJ or 6.2%).[3] Figure1 shows export destination countries and volumes from 2008 to 2025:

The figure shows that while China’s appetite for Australian gas grew steadily until 2021, it began to decline thereafter returning to pre covid levels by 2025. By 2025, China had decided it did not want over dependence on Australia as a source of LNG. Concurrently, it was able to increase domestic production and take advantage of cheap gas originating in Russia delivered over the Power of Siberia pipeline.[4]

China’s new energy calculus and a more competitive global market for LNG have resulted in a decline in Australian LNG exports. Global LNG Hub reported in December 2025, that Australian LNG exports had ’slipped again’ in 2025, with year-to-date shipments down 2.8% compared with the same period in 2024.[5] It further concluded that the slowdown left Australia further behind the US and Qatar, which have expanded output and strengthened their positions in the global LNG market.[6] Global LNG trade grew 5.2% y/y in the first ten months of 2025, but Australian LNG volumes fell to 65.8 Mt, down from 67.7 Mt in the previous year — highlighting Australia’s continuing supply stagnation.[7] Global LNG Hub concluded that:

With US LNG capacity surging, Qatar expanding long-term supply, and China reducing Australian purchases, Australian LNG risks losing further global market share in 2026 unless new investment or upstream improvements materialise.[8]

Wobbles in the market for Australian LNG have drawn the attention of Australian Governments and created a context for efforts to diversify and reset Australia’s overseas markets for gas. As it seeks to reset, Australia is attempting to leverage its relationship with Japan, which has become the largest and most important buyer of Australian LNG. Relative to the first ten months of 2024, Japan increased its intake of Australian LNG by +4.7% y/y 2023-2025 to 22.2 Mt, reaffirming its position as Australia’s top buyer.[9] While only partially offsetting the decline in deliveries to China, South Korea provided some encouragement to Australian gas producers increasing with imports to a record 12.5 Mt in the first ten months of 2025.[10]

Australian Government anxiety over the future of Australian gas in Asia has been compounded by regional acceptance of the need to grow renewables. As Australia seeks to grow new markets for Australian gas, it must reckon with regional momentum towards energy transition. Milestones include The ASEAN Vision 2045 and the ASEAN Plan of Action for Energy Cooperation (APAEC), both of which place strong emphasis on clean energy deployment. Eight of ten ASEAN member states have announced net zero emissions targets.[11]

The perceived urgency of growing existing markets and finding new ones is also being driven by declining domestic demand for gas. In the double game played by Labor, decarbonisation of the Australian economy and households messages against gas. By virtue of parity pricing, gas is also an expensive fuel stock for power generation and a major contributor to increased power costs for industry and consumers. In 2026, grid decarbonisation from renewables and batteries, coupled with increased electrification of industry and households, is eating into traditional Australian markets for gas. In its March 2026, Gas Statement of Opportunities, AEMO points to near term improvements in supply conditions in the domestic market.[12] Where States are pursuing decarbonisation of households and industry more aggressively, domestic markets for gas are experiencing the greatest impacts. In Victoria, AEMO expects “annual gas production and daily supply capacity is forecast to fall 52.8% and 35.2% by 2030, respectively, with annual consumption to reduce by 10.5% over the same period.”[13]

Friends in need: The Role of Japan

As Australian Governments preach the benefits of renewables to Australians, it is a very different narrative that is heard behind closed doors in Asia. To offset decline in exports to China and downward pressure on demand from the energy transition, Australian Governments are pulling all available levers to create new markets for Australian gas, as well as to expand existing ones. In this quest, Australian Governments are seeking to leverage our special relationship with Japan in South East Asian markets.

With China’s waning enthusiasm for Australia’s LNG, Japan has become our biggest customer. Japan’s role spans consumption, resale, finance, investment, technology and expertise. In 2026, Japan is a:

- large domestic consumer of Australian gas;

- major re-seller of Australian LNG into Asian markets. In 2024, Japanese companies resold more LNG to third countries (at least 600–800 PJ) than they imported directly for domestic use. Australia supplied 41% of resold cargoes;[14]

- major investor in Australian LNG production;[15]

- major financier of gas infrastructure in South East Asia; and

- major supplier of technology and expertise.

Japan’s relationship with Australian LNG is highly profitable and places it at odds with the energy transition in the South East Asian region. Review of the data shows that Japan is actively working with Australian Governments to influence technology choices in the region in favour of gas. Japan is also engaged with almost every stage of the value chain ranging from production to export and consumption. According to Global Energy Monitor:

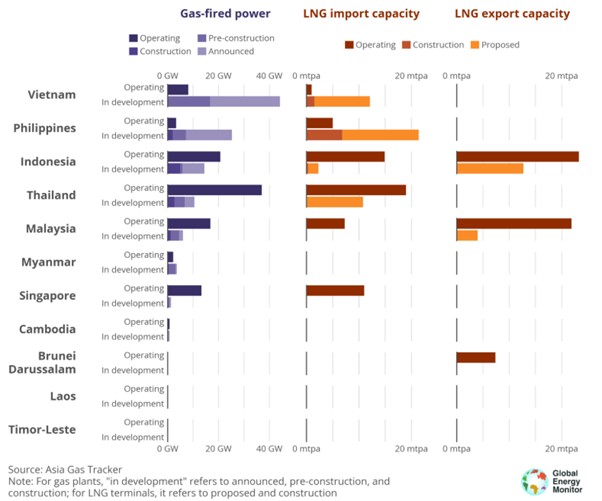

Current gas expansion plans could lead to a doubling of Southeast Asia’s gas-fired power capacity and an 80% increase in its liquefied natural gas (LNG) import capacity. If built, these projects could lock Southeast Asian countries into relying on an economically volatile and insecure fuel and would require a capital investment of over $220 billion.[16]

Global Energy Monitor tracks operating and proposed gas fire power and LNG import/export capacity. Figure 2 describes operating, under construction and proposed LNG investment in South East Asia:

As Figure 2 shows, the gas build out is concentrated in Vietnam, the Philippine’s, Malaysia, Indonesia and Thailand. According to CEED, four Japanese banks, Japan Bank for International Cooperation (JBIC), Sumitomo Mitsui, Mizuho Financial Group, and Mitsubishi UFJ, are among the ten biggest financiers of gas in Southeast Asia, with a combined funding of USD 9.7 billion over the last decade. Part of the impetus for this support seems to be an attempt to shore up Japan’s own energy security and to help utilities offload excess LNG cargoes when they are over contracted.[17] Financing of capacity building also enables Japan to exert influence and control over regional governments, that might otherwise fall within the sphere of Chinese influence.

Hawking Australian gas

The marketing and expansion of Australian gas to South East Asia in collaboration with the Japanese is a top priority for the Cook (WA) and Albanese (FED) Labor Governments. Supply chain embedding of the relationship with Japan begins with production in Australia. According to the Industry thinktank InfluenceMap, Japanese companies (including INPEX, JERA, Mitsubishi and Mitsui) hold more than USD 50 billion in equity across 13 export projects, representing around 17% of global LNG capacity.[18] The same report estimates that based on projected output, these projects could be associated with annual CO₂ emissions of around 290 million tonnes, a figure comparable to the total annual emissions of countries such as Malaysia, Taiwan, and the Philippines.[19]

The success enjoyed by Japanese companies in production, distribution and consumption of Australian LNG is nurtured and protected by activities of the Australian and Japanese Governments aimed at influencing regional government policy in favour of adopting and expanding the role of gas. In Japan, lobbying by gas industry stakeholders has secured a continuing role for gas as part of Japan’s energy mix out to 2040 with a projected 30-40% of Japan’s power coming from thermal sources.[20] Japan’s Strategic Energy Plan also includes “measures to support LNG trading and demand development across Asia, alongside Japan’s domestic needs.”[21]

In Australia, along with Australian stakeholders, Japanese companies have participated in private meetings and industry groups with the aim of influencing government energy policy in favour of gas. According to InfluenceMap, lobbying activities have promoted the importance of new gas supply and LNG for delivering domestic and regional energy security. They have also raised concerns about negative impacts on the industry from stringent climate regulation.[22] Importantly, lobbying of Australian Ministers by Japanese Governments has shaped Australia’s “future gas strategy”. Released by Federal Minister Madeliene King in 2024, the strategy suggested the need for new sources of gas to meet demand out to 2050 and beyond.[23] In the lead up to release of the strategy, according to InfluenceMap, King met Japanese LNG representatives at least seventeen times.[24]

The lie of gas as a transition fuel

The world is supposed to be decarbonising to avoid catastrophic climate change. To conceal what is clearly happening in violation of commitments to reduce emissions (such as the Paris Agreement), the Australian and Japanese Governments have settled on a deception. Gas is required as a transition fuel to a renewable, clean energy world.

WA’s Premier Roger Cook is a big fan. In interviews and industry forums, Cook relies on talking points that closely resemble those of Woodside and Japanese stakeholders. These talking points emphasize the role of gas as a transition fuel. In comments made in mid-2025 to Guardian Australia in Japan, Cook declared that stakeholders in Japan told him the country needed LNG to achieve its target of reducing coal to 19% of its energy mix by 2030, down from 32% in 2019:

What they’re saying to us is that they’re committed to the energy transition towards renewables, getting out of fossil fuels, but they can only do that via LNG as part of the overall energy mix.[25]

Transition can mean different things to different people, but in a 2025 Deloitte report, ironically commissioned by the WA Government, Deloitte found that increasing fossil gas use in Asia for electricity generation was problematic:

There are substantial risks that natural gas could crowd out investments in renewable technologies or delay the broader adoption of zero emission energy systems.[26]

Deloitte’s findings mirror those of Australia’s national science agency (CSIRO). In a report commissioned by oil and gas giant Woodside in 2019, it found increasing gas supply to Asia could have "no change" or "no net benefit" in reducing emissions in most cases.[27]

Global climate science and policy institute, Climate Analytics, has also poured cold water on the idea of gas as a transition fuel. In response to the Deloitte Report and claims made by Roger Cook, CEO and Senior Scientist, Bill Hare declared that there was “no scientific basis “ to the claim that maintaining gas exports was critical to the clean energy transition.[28] The crowding out of renewables is not the only problem. The science is unequivocal that gas is not a clean energy source. According to Climate Analytics, between 2010 and 2019:

gas was the largest source of the increase in CO2 emissions (42%). It’s also responsible for the largest share of methane emissions from fossil fuel production – which is an incredibly potent, but short-lived greenhouse gas that accounts for a substantial amount of warming to date.[29]

Gas at the crossroads: The Iran War

The Iran War is shaping up to change the status quo on gas in southern and south east Asia. When the war commenced on February 28, 2026, LNG markets in South East Asia began to be disrupted by supply shortages and soaring energy costs. According to the US Energy Information Administration, 80% of the oil and LNG that transits through the Strait of Hormuz is heading for Asian markets:

Four Asian economies – China, India, Japan and South Korea – account for 75% of oil and 59% of LNG flows through the chokepoint. Bangladesh, Pakistan and Taiwan are also among the top destinations for LNG shipped through the vital waterway. Within south-east Asia, Thailand and Singapore are the largest importers of LNG from the Middle East.[30]

These economies face major disruption from fossil fuel shortages, including LNG. The longer the war goes on, the greater the disruption. The Oxford Institute for Energy Studies (OEIS) has modelled the impact of the closure of the Strait of Hormuz on global gas markets. In a study released in 2025, OEIS concluded that markets for LNG will diversify to reduce risk from the Middle East. This will likely involve higher demand in the short to medium term from Australian and other suppliers. OEIS forecast that LNG supply from the Middle East would be 110bcm lower on annual basis but that this decline would partly offset by higher volumes from Australia and North America, resulting in an overall decline of 86bcm equivalent to some 15 percent of 2024 global LNG supply.[31] Australia is not the only regional player that could move to exploit new regional opportunities created by diversification. Countries with LNG export capacity constructed or planned such as Indonesia and Malaysia will likely also seek to expand regional export opportunities. Vietnam which has undeveloped reserves may elect to develop these reserves.

If OEIS is correct, South East Asia’s diversification push will increase pressure on Australian Governments to approve new gas projects based on conventional (LNG) and unconventional (fracked) gas reserves. Encouragement to build new capacity also comes from the success enjoyed by Australia in leveraging LNG exports to protect it’s access to refined petroleum, a tactic that has so far worked to partially mitigate supply side issues with petroleum created by the Iran War and closure of the Strait of Hormuz. With only two functioning refineries, the bargaining power afforded by being a top three LNG exporter, has so far protected Australia from the major disruption and economic chaos that stem from severe fuel storages.

WA is set to be a major player in any expansion of gas with both LNG (Browse) and fracking proposals (the Kimberley) on the table in various stages of approval. Rumour has it that Federal Minister, Murray Watt has his finger on the trigger for Woodside’s Browse Gas Project. Environmental groups, the Greens and the Climate Council have labelled the project a “carbon bomb.”[32]

But there is another countervailing narrative. As supply and soaring energy prices point to the economic sense of reducing exposure to gas, nations with no reserves and supply chain exposure might also choose to accelerate electrification and the transition to renewables. Since the beginning of the Russia Ukraine War, Europe has been reducing its exposure to gas. In 2025, the European Union generated more electricity from wind and solar than fossil fuels for the first time.[33] New impetus has been supplied by the Iran War. As the war enters its second month, France has announced its intention to use surpluses of tax revenue from the sale of fossil fuels, to fund a broad plan for electrification and decarbonisation.[34]

South East Asia is also contemplating accelerating its transition. In a 2025 electricity demand review, International Energy Agency (IEA) estimated that South East Asia had 20 terawatts of untapped solar and wind potential, equivalent to around 55 times the region’s current total power capacity.[35] Untapped renewables capacity and vulnerability to economic shocks from fossil fuel dependency, all point toward the need to double down on electrification and renewable energy. Analysts Wood Mackenzie see momentum for renewables building across the region with “higher tariff caps for hybrid projects in Vietnam, battery requirements for new renewables in the Philippines, storage auctions in Malaysia, ambitious solar-plus-storage targets in Indonesia and a Singaporean plan to import up to 6 GW of low-carbon electricity by 2035.”[36]

Conclusions

The Cook and Albanese Governments are working to expand global carbon pollution by shoring up and growing Australian exports of LNG. This is largely happening out of sight and out of mind through advocacy and influence that goes largely unreported. Australia’s efforts to re-invigorate its Asian gas markets are also receiving up lift form the Iran War. With South East Asian nations experiencing supply volatility and soaring energy costs, the need to diversify sources of gas in the interests of energy security has become paramount. Regional over reliance on fossil fuels originating in the Middle East and passing through the Strait of Hormuz, is seen as a systemic risk that must be addressed. In the short term, pressures generated by the Iran War could impact Australian Government decision making on the addition of new gas production capacity through contentious, climate busting, carbon intensive projects such as Woodside’s Browse project.

A counter narrative to the march of gas, is that the Iran War has provided a transformational opportunity for South East Asian Nations to re-balance energy systems in favour of electrification with renewables. As Europe has re-configured its energy mix in favour of renewables, so too can South East Asia.

There is a lot resting on which narrative prevails.

ENDNOTES

[1] Influence Map (2026). Corporate Japan’s Role in Promoting Australian Fossil Fuels. p.8.

[2] Institute for Energy Economics and Financial Analysis. (2026). Australian Gas and LNG Tracker. Retrieved from: https://ieefa.org/australian-gas-and-lng-tracker#section2

[3] Ibid.

[4] East Asia Forum. (2025). Power of Siberia 2 reshapes China's energy security calculus. Retrieved from: https://eastasiaforum.org/2025/10/31/power-of-siberia-2-reshapes-chinas…

[5] Global LNG Hub. (2025). Australian LNG exports lose momentum as Japan and Korea increase buying. Retrieved from: https://globallnghub.com/australian-lng-exports-lose-momentum-as-japan-…

[6] Ibid.

[7] Ibid.

[8] Ibid.

[9] Ibid.

[10] Ibid.

[11] International Energy Agency (IEA). (2025). Southeast Asia can harness vast renewable resources to meet fast-growing electricity demand. Retrieved from: https://www.iea.org/news/southeast-asia-can-harness-vast-renewable-reso…

[12] Australian Energy Market Operator. (2026). Near-term gas supply outlook improves, longer-term investment needed. Retrieved from: https://www.aemo.com.au/newsroom/media-release/2026-gsoo

[13] Ibid.

[14] Sier, J. (2025). Major shift in our understanding: Japan resells more Australian Gas. Financial Review. May 20, 2025. Retrieved from: https://www.afr.com/world/asia/japan-ramps-up-regional-reselling-of-aus…

[15] Japanese companies hold $US 50billion in equity across thirteen Australian export projects. Vide InfluenceMap (2026). Corporate Japan’s Role in Promoting Australian Fossil Fuels: How Japanese corporate influence shapes Australian LNG policy, prices and regional dependence. p.3. Retrieved from: https://influencemap.org/briefing/LNG-briefing-34341

[16] Global Energy Monitor. (2024). South East Asia’s Energy Crossroads: The Cost of Gas Expansion Versus the Promise of Renewables. Retrieved from: https://globalenergymonitor.org/report/southeast-asias-energy-crossroad…

[17] Ibid., p.11

[18] InfluenceMap (2026). Corporate Japan’s Role in Promoting Australian Fossil Fuels: How Japanese corporate influence shapes Australian LNG policy, prices and regional dependence. p.3. Retrieved from: https://influencemap.org/briefing/LNG-briefing-34341

[19] Ibid.

[20] Ibid.

[21] Ibid.

[22] Ibid.

[23] Morton, A. (2026). Australian ministers met Japanese gas companies 20 times amid fossil fuel lobbying push. The Guardian Australia. 10 Feb. 2026. Retrieved from: https://www.theguardian.com/australia-news/2026/feb/09/australian-minis…

[24] Ibid.

[25] Jervis-Brady, D. (2025). Gas belongs to the people’: WA premier Roger Cook urges federal Labor to adopt reserve policy. The Guardian Australia 8 July 2025. Retrieved from: https://www.theguardian.com/australia-news/2025/jul/08/wa-premier-roger…

[26] Ho Cason (2025). Secret WA government report casts doubt on claims domestic gas will help other countries in energy transition. ABC News 6 November 2025. Retrieved from: https://www.abc.net.au/news/2025-11-06/wa-government-gas-industry-energ…

[27] Hayward, Jenny; Graham, Paul. Modelling the emission impact of additional LNG in Asia. Client: CSIRO; 2019. csiro:EP197155. https://doi.org/10.25919/0kpd-8g59

[28] Jervis-Brady, D. (2025). Op.cit.

[29] Climate Analytics. n.d. Gas Phase Out. Retrieved from: https://climateanalytics.org/projects/gas-phase-out

[30] Green Central Banking. (2026). ‘Clean Energy, not LNG’ is Asia’s best hedge against energy shocks. Retrieved from: https://greencentralbanking.com/2026/03/09/clean-energy-not-lng-is-asia…

[31] Oxford Instutute for Energy Studies. (2025). Closing the Strait of Hormuz: Impact on the Global Gas Market. p.6. Retrieved from: https://www.oxfordenergy.org/publications/closing-the-strait-of-hormuz-…

[32] Climate Council. (2024). Only one right answer now for WA “climate bomb” project. Retrieved from: https://www.climatecouncil.org.au/resources/only-one-right-answer-wa-cl…

[33] Kurlantzick, J. (2026). The Iran War Is Reshaping Asia’s Energy Security Strategies. Retrieved from: https://www.cfr.org/articles/the-iran-war-is-reshaping-asias-energy-sec…

[34] Le Monde. (2026). The government intends to accelerate electrification and a gradual phase-out of hydrocarbons. Retrieved from: https://www.lemonde.fr/energies/article/2026/04/01/le-gouvernement-ente…

[35] International Energy Agency. (2025). Southeast Asia can harness vast renewable resources to meet fast-growing electricity demand. Retrieved from: https://www.iea.org/news/southeast-asia-can-harness-vast-renewable-reso…

[36] Wood MacKenzie. (2026). Middle East conflict to have limited near-term impact on Southeast Asia power markets but raises long-term energy security risks. Retrieved from: https://www.lexology.com/library/detail.aspx?g=c9d499d2-3737-4491-9a7f-…

Header photo: Image courtesy of Kuntum Kuro and Pexels. Licensed under Creative Commons. (https://www.pexels.com/de-de/foto/wasser-segeln-schiff-tanker-18115096/)

[Opinions expressed are those of the author and not official policy of Greens WA]